To be deductible, a business expense must be both ordinary and necessary. An ordinary expense is one that is common and accepted in your field of business. A necessary expense is one that’s helpful and appropriate for your business.

The IRS sometimes challenges deductions claimed for certain types of business expenses. In doing so, an examiner might claim that payments made by a corporation to a shareholder for personal items or that are above or below fair market value constitute “constructive dividends.” Reclassifying business expenses as dividends has adverse tax consequences, as a recent case demonstrates.

No Deduction for Dividends

Typically, a successful corporation pays out dividends to its shareholders, based on earnings for the year. The exact amount of dividends a shareholder receives depends on his or her proportionate share in the company. These dividends are declared by the company on a specified date and then paid out in cash or reinvested in more shares for the shareholder.

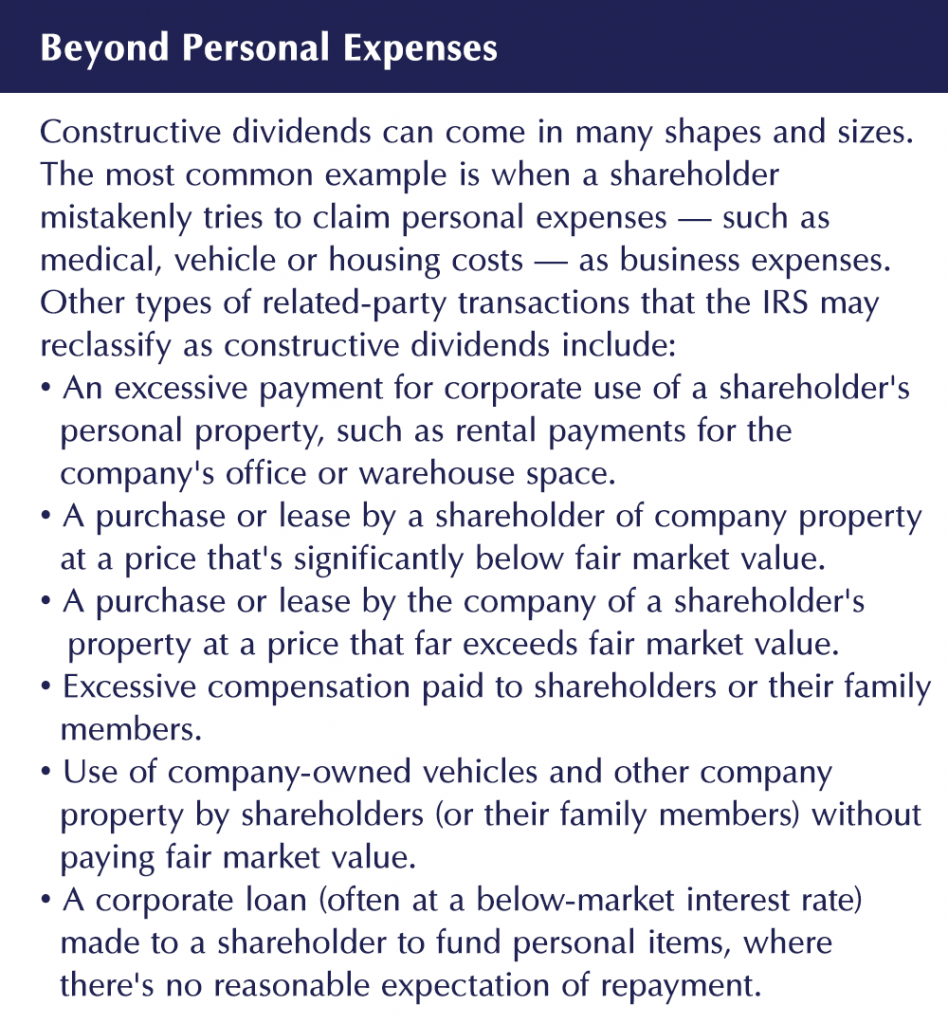

However, a corporation may make other payments to one or more shareholders, which the IRS might classify as “constructive dividends.” This often happens when owners of a closely held business use corporate funds to pay personal expenses. But it can also occur at multibillion-dollar conglomerates, and it may involve more than just running personal expenses through the business. (See “Beyond Personal Expenses” below.)

The crux of the matter is: Owning all (or part) of a company doesn’t give you the unrestricted right to pay and record expenses in the manner in which you see fit. Notably, you must follow tax rules and restrictions.

Tax Consequences

From an income tax perspective, dividends paid out by corporations are taxable to shareholders at the personal level. Qualified dividends received by a C corporation shareholder are taxable at the same preferential tax rates as long-term capital gains. Currently, the maximum tax rate for qualified dividends is 15% (20% if you’re in the top ordinary income tax bracket).

On the downside, dividends can’t be deducted by the corporation. So, dividends are paid using after-tax dollars, meaning they’re effectively taxed twice.

Compensation and most other types of payment (such as consulting or management fees) are taxable to shareholders at ordinary income tax rates. However, these legitimate expenses are usually fully deductible by the company (unless they aren’t at arm’s length). As a result, depending on its circumstances, a corporation may try to disguise dividends as compensation or some other type of payment.

This is where the IRS could jump into the fray. If it treats a payment as a constructive dividend, the business deduction the corporation tried to claim for that payment (for example, a compensation deduction) is disallowed, thereby increasing its tax liability. Furthermore, the IRS may impose penalties and interest for tax underpayments. If the company’s owners purposely evaded their tax responsibilities, they may face criminal sanctions.

For the shareholders, constructive dividends are taxable as ordinary income. However, unlike compensation, a dividend payment isn’t subject to payroll taxes. Therefore, the overall tax results for shareholders will vary.

Case in Point

The IRS is likely to step in if it perceives that a company is paying personal expenses on behalf of shareholders. That was the main issue presented to the U.S. Tax Court in one case. (Luczaj & Associates v. Commissioner, T.C. Memo 2017-42, March 8, 2017)

The taxpayers, a married couple residing in California, owned a C corporation. The husband held 51% of the stock, and the wife owned 49%. The wife was the company’s sole employee during the tax years in question, while the husband worked full time as a high school adult transition coordinator, supervising and teaching special needs students.

The corporation was engaged in the business of originating home mortgages, acting as an independent contractor for California Mortgage Group (CMG). Its main function was to solicit clients for CMG. After the company referred clients to CMG, they offered those individuals help with the purchase of homes.

The wife’s sole responsibility was client recruitment for CMG. She had a desk in CMG’s main office in California, where she worked at least two days a week. She testified at trial that she worked from home the rest of the week and typically met clients at home or in a public place.

For the two tax years in question, the corporation claimed deductions for a wide variety of expenses, including travel, entertainment, insurance, telephone, advertising, gifts, medical expenses, utilities, maintenance, depreciation, dues and subscriptions. Some of these expenses included repairs to the couple’s personal residences, swimming pool costs and personal entertainment expenditures.

The IRS contested most of the reported business expenses due to lack of substantiation or lack of business purpose. It argued that the payments constituted constructive dividends to the shareholders. Finally, the IRS imposed accuracy-related penalties for the tax years in question.

The Tax Court agreed with the IRS. The court determined that many of the expenses the business claimed as marketing and promotional expenses were actually payments of personal expenses that directly benefited the shareholders. For instance, the wife claimed 100% business use of two vehicles, but didn’t follow IRS procedures for documenting business use. The court also ruled that payments may be treated as constructive dividends without the corporation making a formal declaration of dividends.

The Bottom Line

It’s easy to run afoul of the IRS on this issue. Businesses should always keep detailed, contemporaneous records to support deductions and other tax positions, especially when it comes to transactions with related parties.

The IRS generally won’t, for example, treat a payment as a constructive dividend if the company can demonstrate that it lacked sufficient earnings to pay dividends or that a payment was, in fact, used to pay ordinary and necessary business expenses, rather than personal expenses.

In some instances, expenses may fall into a “gray area” where you’re unsure of the appropriate tax treatment. Do you have questions? We can help. Fill out the form below the “Beyond Personal Expenses” box.

Contact Us

© 2024 CPA Site Solutions.

Disclaimer of Liability

Our firm provides the information in this article for general guidance only, and does not constitute the provision of legal advice, tax advice, accounting services, investment advice or professional consulting of any kind. The information provided herein should not be used as a substitute for consultation with professional tax, accounting, legal or other competent advisors. Before making any decision or taking any action, you should consult a professional advisor who has been provided with all pertinent facts relevant to your particular situation. Tax articles in this blog are not intended to be used, and cannot be used by any taxpayer, for the purpose of avoiding accuracy-related penalties that may be imposed on the taxpayer. The information is provided “as is,” with no assurance or guarantee of completeness, accuracy or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability and fitness for a particular purpose.

Blog

Nonprofit Insights