Cash as a form of legal tender isn’t yet as obsolete as 8-track tapes and VCRs. But it’s definitely less popular with certain demographic groups than others.

Only 30 percent of all retail transactions were completed using cash in 2018, down from 40 percent in 2012, according to the Federal Reserve. And that trend is expected to continue, causing some retailers to stop accepting cash from customers.

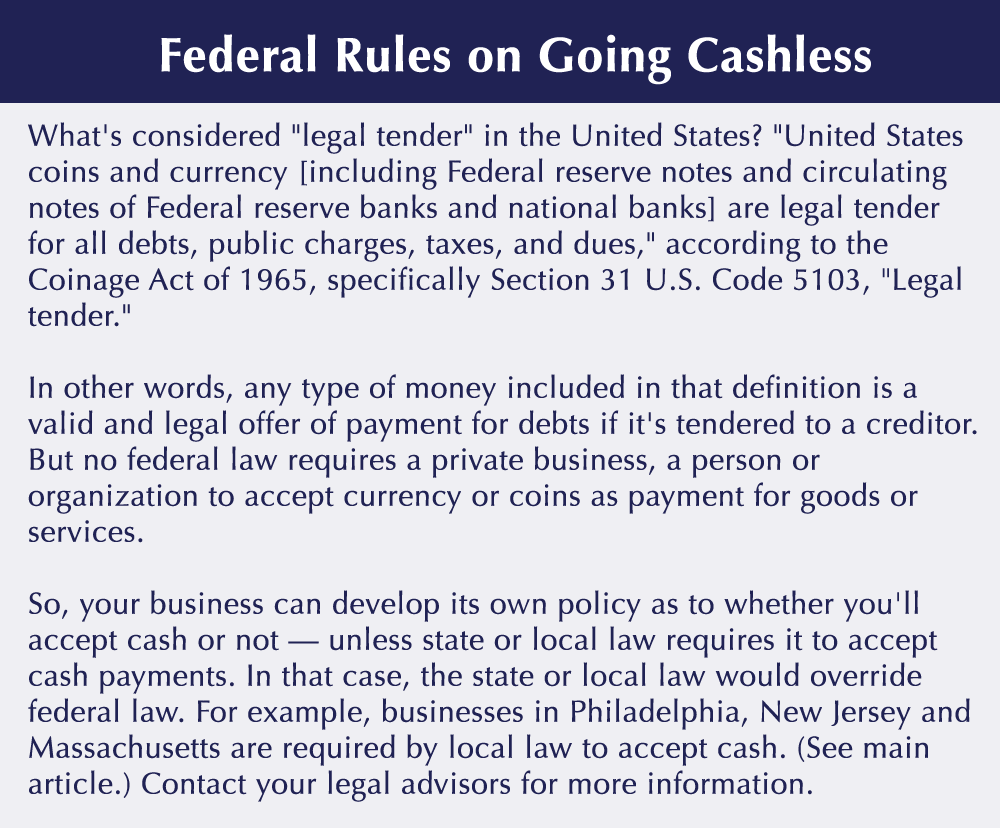

Is it legal to refuse cash payments — or even a smart business practice? It depends on where you’re located. In February, for example, Philadelphia’s city council passed an ordinance that requires businesses to accept cash, except for orders placed online or by telephone. The law comes amid plans announced by online retailing giant Amazon to open cashless brick-and-mortar stores around the country.

Some other local and state governments may follow Philadelphia’s lead. Here’s what retailers should know about the cashless movement.

Sign of the Times

When is the last time you paid cash for groceries, gasoline or even a pack of gum? The answer probably depends on your age and income level. Generation Xers, Millennials and even Generation Zers tend to be more comfortable swiping their credit or debit cards or tapping Venmo or Google Pay than they are paying for goods and services in greenbacks and spare change.

Going cashless isn’t preferred by all Americans, however. Many middle-aged consumers and senior citizens are still more comfortable paying with cash than swiping a credit card or setting up a digital wallet. And some low-income patrons can only pay with cash, because they don’t have credit cards or bank accounts — or smartphones and the requisite identification to qualify for digital payment.

That’s why the Philadelphia city council stepped in when several retailers started to refuse cash payments. “There’s a reasonable segment of people who wouldn’t be able to patronize those stores because they don’t have any kind of credit or debit card,” said Philadelphia Councilman Bill Greenlee after introducing the bill to require cash payments. He argued that, by refusing to accept cash, retailers were sending the message that they didn’t want to do business with low-income or immigrant customers who don’t have bank accounts or an established credit history.

Why Go Cashless

Even though going cashless may turn away some customers, some store owners have decided that cash is more trouble than it’s worth. They argue that handling cash is costly and time consuming. For example, it requires managers to:

- Tally up cash receipts and count cash registers between shifts and at closing,

- Make regular cash deposits at the bank and

- Implement physical controls over cash (such as lockboxes, safes and surveillance cameras).

Plus, cash is susceptible to theft and fraud. And some customers will spend less if they’re limited to the cash in their pockets than if they use a credit card. Some restaurants even say they don’t accept it, in part, because it’s dirty.

By comparison, credit or debit cards and other digital alternatives are more convenient — just swipe, insert or tap, and then go. In addition, cashless payment forms facilitate sales and can dramatically reduce the chance of theft — if the retailer has adequate cybersecurity measures in place to prevent hackers from accessing customer data. In fact, several large retailers, including Starbucks and Walmart, are considering adopting Amazon’s cashless brick-and-mortar business model.

State of the Union

Amazon has indicated, off the record, that it won’t put any of its brick-and-mortar stores in Philadelphia, due to the new ordinance. But the City of Brotherly Love isn’t the only place in the country where cash is getting more love.

In March, New Jersey’s Governor Phil Murphy signed into law a measure that prevents retailers from prohibiting cash payments. Bills banning cashless merchants are currently being considered in New York City and Washington, D.C. And Massachusetts has had a similar prohibition on the books since 1978, although the law has seldom been enforced.

Right for Your Business?

Outside of the localities that prohibit a cashless business model, retailers have an important decision to make: Should we still accept cash from customers? There’s no universal “right” or “wrong” answer. Contact your financial and legal advisors to evaluate the pros and cons before jumping on the cashless bandwagon.

© Copyright 2019 Thomson Reuters. All rights reserved. Republication or redistribution of Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. Thomson Reuters and the Kinesis logo are trademarks of Thomson Reuters and its affiliated companies.

Disclaimer of Liability

Our firm provides the information in this e-newsletter for general guidance only and does not constitute the provision of legal advice, tax advice, accounting services, investment advice, or professional consulting of any kind. The information provided herein should not be used as a substitute for consultation with professional tax, accounting, legal, or other competent advisers. Before making any decision or taking any action, you should consult a professional adviser who has been provided with all pertinent facts relevant to your particular situation. Tax articles in this e-newsletter are not intended to be used, and cannot be used by any taxpayer, for the purpose of avoiding accuracy-related penalties that may be imposed on the taxpayer. The information is provided “as is,” with no assurance or guarantee of completeness, accuracy, or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability, and fitness for a particular purpose.

Blog

Nonprofit Insights