Let’s explain a few terms.

Definitions

Passive income: money coming in that you don’t actively work for. In other words, things like rental properties, dividends and K-1s (return on investments).

Passive losses: money you lose on things like investments and property. For example, your rental expenses exceed the income for the year. Or you have a loss flowing through from an investment you made in a friend’s business.

Active Income: income you make at your “regular” job. For example, your W-2 wages or Schedule C trade or business income.

Material participation: any work you perform that is regular, continuous and [you have a] substantial involvement in a trade or business (or rental real estate activity for real estate professionals).

Why Does This Matter?

In a nutshell, it could reduce your tax liability.

Since you can only deduct passive losses if you have passive income to offset it, you want to make sure your income is classified appropriately.

For example, you actively participate in a S-Corp. You also own a building personally that you rent back to the S-Corp. In this instance, both the S-Corp and self-rental may be treated as active. If you had rented the building to an unrelated lessee with zero participation, the rental would be treated as passive.

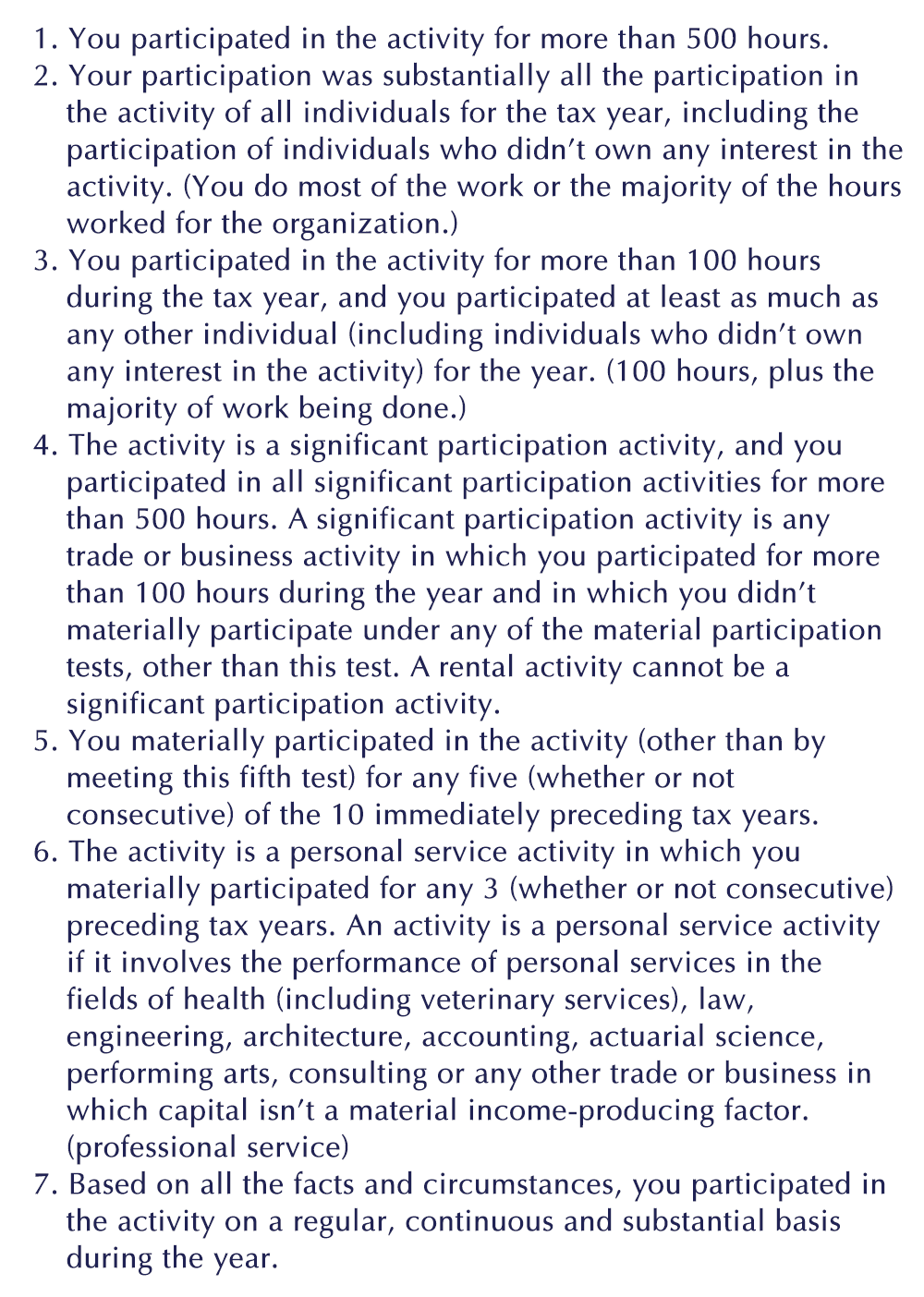

This all has to do with the Passive Activity Limitations (PALS) and it can be complicated. In fact, the IRS has established that when any one of the seven tests are met a taxpayer materially participates in an activity. (see text box below)

Real Estate Professionals

Generally, rental activities are passive activities even if you materially participated in them. Some taxpayers may qualify as real estate professionals. Real estate professionals have to meet BOTH the material participation rules and the real estate professional rules outlined below.

IRS Rules for Real Estate Professionals

1. More than half of the personal services you performed in all trades or businesses during the tax year were performed in real property trades or businesses in which you materially participated. (At least half of your time has to be in real estate.)

2. You performed more than 750 hours of services during the tax year in real property trades or businesses in which you materially participated.

Bottom line

You can reduce your tax liability if you meet criteria outlined by the IRS. There are many investors and real estate professionals who meet these qualifications and don’t realize it. We’re here to help. Fill out the form below and we’ll reach out to you.

Seven Tests:

Contact Us

Blog

Nonprofit Insights