Is your business part of the global economy? If not, it may be losing out on some revenue- and value-building opportunities. However, “going global” obviously isn’t as simple as snapping your fingers and tapping into new markets. And it isn’t necessarily right for every business. Here are several challenges the international marketplace can bring, along with a systematic approach to help your venture succeed globally.

Overcoming Challenges

Should you expand your business overseas? Just because you’ve thrived in the United States doesn’t mean you’ll achieve the same sort of results internationally. You don’t want to damage your core business by exhausting resources elsewhere.

Take a hard and honest look at your financial picture. Do you have the capital to support the initial investment and then grow through what could be a lengthy process? If the answer is “yes,” it may be time to take the plunge. But remember that you probably won’t be an overnight success.

Analyze whether there’s a distinct need for your products or services in the countries you’re targeting. Most important, be prepared to meet these six challenges head on:

1. Language and culture.

If you’re looking to expand into markets where English isn’t the first language, you’ll need people who can translate fluently. Also, realize that the culture, both business and personal, can be quite different in a foreign country.

2. Compliance and regulations.

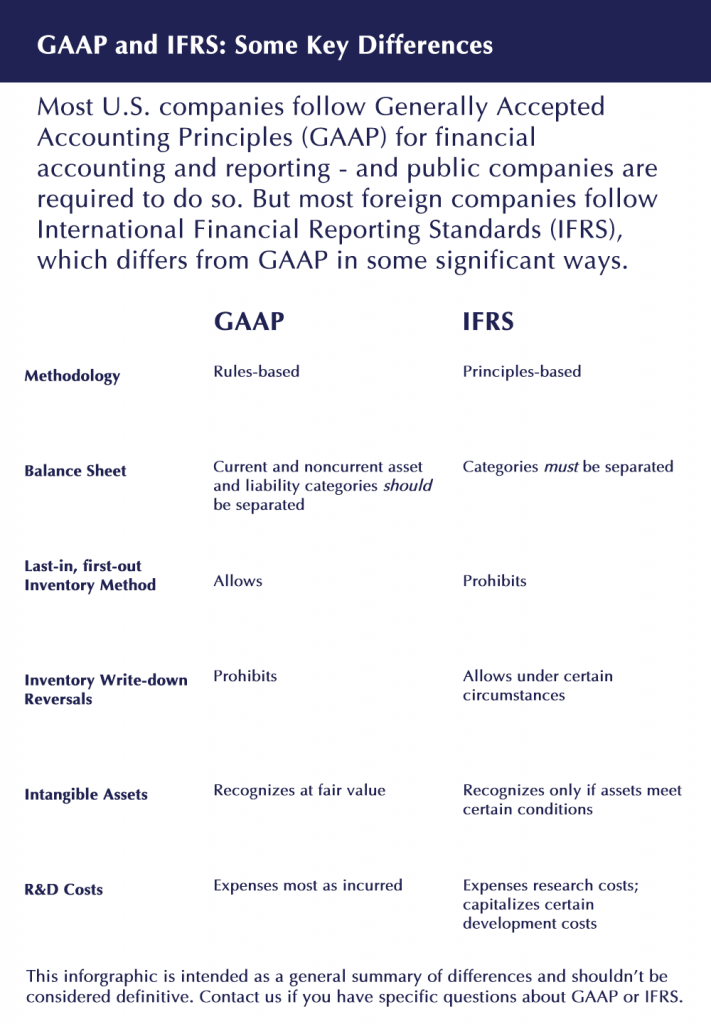

Different rules, standards and regulations apply in foreign countries — even if they seem similar to those of the United States. Coping with legal differences can be unnerving to the unprepared. Something as simple as establishing a corporation can be a trying process overseas. Contract with qualified legal, accounting and banking advisors to help you understand and adhere to the rules.The financial reporting norms and practices also may differ abroad. For instance, lenders in foreign markets might request financial statements that conform to the international accounting rules, rather than those used in the United States. (See “GAAP and IFRS: Some key differences” below.)

3. Packaging.

Packaging requirements vary from country to country. For instance, in the United States, you might have to provide instructions only in English and Spanish. But products marketed regionally could require directions in multiple languages — up to two dozen in some parts of Europe.

4. Business environment.

If you want to do business in foreign countries, you may need to become accustomed to a slower pace of life and more regulatory red tape. Remember to stay patient and follow local policies and procedures. As you gradually build trust, the pace may pick up.

5. Local competition.

How can you convince customers in foreign countries to choose your goods? Global giants (like Amazon) have more clout. As a smaller business, you’ll have to work hard to show that your products have value and are superior to local offerings.

6. Taxes.

One of the biggest challenges of expanding into foreign markets is the complexity of the tax rules for global businesses. Similar to operating in multiple U.S. states, a global business may owe income tax, sales tax, property tax and other assessments in the countries where it sells products and services.

Historically, some U.S. businesses have decided to expatriate to countries with lower tax rates to save taxes. However, businesses with global operations face complex new tax rules under the Tax Cuts and Jobs Act (TCJA).

In general, under the TCJA, there’s an incentive for businesses headquartered outside of the United States to repatriate, as well as to bring cash being held overseas back to the United States. Your tax advisor can help your business comply with the complex global rules and devise strategies to help minimize taxes.

Adopting a GLOBAL Approach

If you’re ready to take the plunge into overseas markets, we’ve compiled these tips — arranged using an easy-to-remember acronym: GLOBAL — to help you succeed.

Go on a fact-finding mission

Run through all possible financial scenarios: worst, best and probable. Spend considerable time in the foreign country or countries where you want to branch out and conduct thorough due diligence. Consider visiting potential customers, distributors, partners and competitors. The information gathered can provide valuable insights into how to manufacture, distribute, price and promote your products in foreign markets.

Look for reliable business partners

Consider teaming up with others, like an established local business, or finding a local mentor. Seek out people who understand the market, speak the language and know how to deal with local regulations. A partnership can improve efficiency and help promote your company’s brand in a way that’s meaningful to the target market.

Be cautious about rushing into strategic alliances that can bind you indefinitely, however. While a partner may appear to be a good choice today, a better one might emerge tomorrow. And don’t assume that biggest is always best. A smaller distributor may devote more attention to your cause than a larger one would.

Organize your business plan

You can’t go into global expansion without a plan. This includes creating an infrastructure that facilitates a smooth launch. Coordinate efforts at home and abroad, and then determine which business decisions can be made on a local level and which need to be made centrally.

Assemble a management team that can implement your strategies from a remote office. Set up IT and telephone systems for optimal use. And establish policies and procedures for secure data sharing and storage that also comply with legal obligations.

Brainstorm globally

Think beyond how new ideas will fare in the United States. If you’re going to launch a new product, also consider how it will sell in the foreign markets that you’re pursuing. Companies with global mindsets evaluate such issues as time zones, language and culture. Failure to address these concerns early may lead to delayed launches and insulted international business partners.

Adapt to changes

Expect that there will be some bumps in the road to global success. Be ready to shift gears if a different approach is needed. Focus on consumer demand rather than traditional strategies that have previously worked for you in the United States.

Listen to outside experts

Entrepreneurs tend to be self-reliant, but everyone can use some help expanding in global markets. Though it may be difficult to concede some control, you can’t do (or know) everything, especially in a foreign market.

Right out of the starting gate, you’ll need legal, tax and accounting experts to help set up your business, package its products, report its financial results, comply with local labor regulations and file its taxes. These experts’ fees often pay for themselves by reducing stress, lowering tax obligations and avoiding inquiry from foreign regulatory bodies.

Ready, Set, Go Global

Going global is probably one of the biggest decisions you’ll make in your business. If you make the jump, thorough due diligence and a methodical GLOBAL approach can help ensure you land on your feet and keep running the race. Partner Glenn Lankford is an expert in international taxation. Contact him today for assistance, 434.296.2156.

Contact Us

© Copyright 2019 Thomson Reuters. All rights reserved. Republication or redistribution of Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. Thomson Reuters and the Kinesis logo are trademarks of Thomson Reuters and its affiliated companies.

Disclaimer of Liability Our firm provides the information in this e-newsletter for general guidance only, and does not constitute the provision of legal advice, tax advice, accounting services, investment advice or professional consulting of any kind. The information provided herein should not be used as a substitute for consultation with professional tax, accounting, legal or other competent advisers. Before making any decision or taking any action, you should consult a professional adviser who has been provided with all pertinent facts relevant to your particular situation. Tax articles in this e-newsletter are not intended to be used, and cannot be used by any taxpayer, for the purpose of avoiding accuracy-related penalties that may be imposed on the taxpayer. The information is provided “as is,” with no assurance or guarantee of completeness, accuracy or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability and fitness for a particular purpose.

Blog

Nonprofit Insights